In all likelihood, would the chance of printing presses around the world operating in full capacity getting a bit less?

Who can guess what's the real inflation in China?

What is to happen to Spain? anyone after Spain?

EUR, are you still there?

Equity, equity, equity, is it going to be a good year for equity? or commodity still?

Bond, bond bubble still blowing?

Gold is gold. Has everyone already got a piece? then what?

Monday, December 20, 2010

Sunday, October 10, 2010

More currency and trade - G20

From weekend G20 meeting, now it's head-on between developed world (largely US and Euro zone) and emerging markets.

Tim Geithner:

“The IMF must strengthen its surveillance of exchange-rate policies and reserve accumulation practices,” he told the IMF’s ministerial steering committee. “[E]xcess reserve accumulation on a global scale is leading to serious distortions in the international monetary and financial system, and is inhibiting the international adjustment process.”

Zhou Xiaochuan:

"The continuation of extremely low interest rates and unconventional monetary policies by major reserve currency issuers have created stark challenges for emerging market countries in the conduct of monetary policy,” he said.

“The Fund’s current surveillance framework, which focuses on exchange rate policies, effectively leaves developed countries outside the Fund’s oversight.”

Currency is politics. Since Bretton Wood, the US government perfected it... unfortunately when you are using it for too many times, others will eventually be fed up.

My bet is neither side will back off on its position.

Tim Geithner:

“The IMF must strengthen its surveillance of exchange-rate policies and reserve accumulation practices,” he told the IMF’s ministerial steering committee. “[E]xcess reserve accumulation on a global scale is leading to serious distortions in the international monetary and financial system, and is inhibiting the international adjustment process.”

Zhou Xiaochuan:

"The continuation of extremely low interest rates and unconventional monetary policies by major reserve currency issuers have created stark challenges for emerging market countries in the conduct of monetary policy,” he said.

“The Fund’s current surveillance framework, which focuses on exchange rate policies, effectively leaves developed countries outside the Fund’s oversight.”

Currency is politics. Since Bretton Wood, the US government perfected it... unfortunately when you are using it for too many times, others will eventually be fed up.

My bet is neither side will back off on its position.

Saturday, October 9, 2010

More currency and trade

Douglas A. Irwin, the Professor at Dartmouth College write a piece on Wallstreet Jounal:

On infation, he wrote

"The great concern is that an expansionary monetary policy will lead to uncontrolled inflation, destroying faith in the dollar. Similar sentiments were expressed in the 1930s by advocates of "sound money" who opposed going off the gold standard. Such fears may be justified in ordinary times of full employment, but when there is considerable slack in the economy and unemployment remains high, monetary policy can help to raise output before it leads to higher prices."

Sure enough that's the solution Feb is seeking. However before the US finally raises output the rest of the world may have been inflated to the moon.

Related stories:

Brazil doubled tax on currency transaction - a "Tobin tax" and other currencies Korea/India/Philippines/Indonesia/Thailand/Japan

http://www.bloomberg.com/news/2010-10-05/currency-controls-tighten-as-korea-audits-banks-brazil-doubles-bond-tax.html

Goodbye, Free Trade?

High tariffs and currency wars cost us big in the 1930s. We can avoid making the same mistakes again.

http://online.wsj.com/article/SB10001424052748704696304575538573595009754.htmlOn infation, he wrote

"The great concern is that an expansionary monetary policy will lead to uncontrolled inflation, destroying faith in the dollar. Similar sentiments were expressed in the 1930s by advocates of "sound money" who opposed going off the gold standard. Such fears may be justified in ordinary times of full employment, but when there is considerable slack in the economy and unemployment remains high, monetary policy can help to raise output before it leads to higher prices."

Sure enough that's the solution Feb is seeking. However before the US finally raises output the rest of the world may have been inflated to the moon.

Related stories:

Brazil doubled tax on currency transaction - a "Tobin tax" and other currencies Korea/India/Philippines/Indonesia/Thailand/Japan

http://www.bloomberg.com/news/2010-10-05/currency-controls-tighten-as-korea-audits-banks-brazil-doubles-bond-tax.html

The government printing press

Financial times has in the past week a few articles talking about "currency war"

http://www.ft.com/cms/s/0/da5dfb94-d30a-11df-9ae9-00144feabdc0.html

and see other related links.

Financial investors since 2 years ago have entered a roller-coaster ride and up until today had at least both the down and up phase... thrilling and pleasant to some... there are more tricks to come, definitely... let's pray not to fall out of the chair.

This time round, though, anyone who observed market closely may have to agree that ever since the play got out of control of the free-wheeling American (more precisely Wall Street) capitalist, central bankers have taken over the driving seat. As central bankers cranking up their printing presses and getting set for the competition, the only way for the financial markets is up, up, and up...

I am still appalled at how far the central bankers are willing to go to fight to make their own endorsed green/yellow/whatever color paper worth less by the day...

Anyway, the ride is far from over so sit tight and enjoy it. Anyway, as of Fri 8Oct:

Gold - 1340

USDJPY - 82

UST 10-yr 2.4%

Emerging market stock index - back to climax, wah hoo! (with the exception of China A share market which is also crawling back)

Commodities, food, and property - you know

Inflation - I feel steamingly hot here... but sadly the one owns the largest printing press is missing the action

Bond - hope you didn't buy the Mexico century bond... 100 years is a looong time... fund managers are telling me to stretch the tenor. I've already stretched it to cover at least 2 cycles of future crisis

Currency - where most actions are happening. keep eyes open wide

9 Oct 10

http://www.ft.com/cms/s/0/da5dfb94-d30a-11df-9ae9-00144feabdc0.html

and see other related links.

Financial investors since 2 years ago have entered a roller-coaster ride and up until today had at least both the down and up phase... thrilling and pleasant to some... there are more tricks to come, definitely... let's pray not to fall out of the chair.

This time round, though, anyone who observed market closely may have to agree that ever since the play got out of control of the free-wheeling American (more precisely Wall Street) capitalist, central bankers have taken over the driving seat. As central bankers cranking up their printing presses and getting set for the competition, the only way for the financial markets is up, up, and up...

I am still appalled at how far the central bankers are willing to go to fight to make their own endorsed green/yellow/whatever color paper worth less by the day...

Anyway, the ride is far from over so sit tight and enjoy it. Anyway, as of Fri 8Oct:

Gold - 1340

USDJPY - 82

UST 10-yr 2.4%

Emerging market stock index - back to climax, wah hoo! (with the exception of China A share market which is also crawling back)

Commodities, food, and property - you know

Inflation - I feel steamingly hot here... but sadly the one owns the largest printing press is missing the action

Bond - hope you didn't buy the Mexico century bond... 100 years is a looong time... fund managers are telling me to stretch the tenor. I've already stretched it to cover at least 2 cycles of future crisis

Currency - where most actions are happening. keep eyes open wide

9 Oct 10

Sunday, June 6, 2010

Euro fear getting deeper

On Friday, headlines were on weak job number and Euro.

May non farm payrolls +431k turned out to be lower than consensus and worse, most of the increase were made up from census job, rather than from private sector.

Euro fear is getting deeper. It's about Hungary. Euro tanked 1.6% during the session and moved below 1.2 for the 1st time since 2005.

Over the weekend, some positive progress on oil spill is reported BP. Its cap system was reported to be capturing 90% of the crude oil gushing from the crack at the sea bed. Should be a good sign on the speculative position on BP and Transocean. Will see on Monday.

Anyway, Hungary shouldn't be the last one in this European domino show which began being played out in March. I still remember vividly the troubles with Ukraine, Turkish banks in the mid of banking crisis in 2009... Hungary is weak, others may not be able to hang on for much longer either...

From Wiki:

Hungary:

- Capital: Budapest (beautiful place. one of the top 15 tourist destinations in the world)

- population: 10m

- GDP 2009: 130b

- joined EU in May 2004

- Privatization wave: The PM started the austerity program in 1995. The government privatization program ended on schedule in 1998: 80% of GDP is now produced by the private sector, and foreign owners control 70% of financial institutions, 66% of industry, 90% of telecommunications, and 50% of the trading sector (doesn't look really pretty to me)

- Real wage growth was negative from 2007. in the midst of 2008 banking crisis, the Hugarian National Bank raised interest to 11.5% and Hugarian Government took a 25.1b rescue package from IMF, EU and World Bank.

Seekingalpha/David White

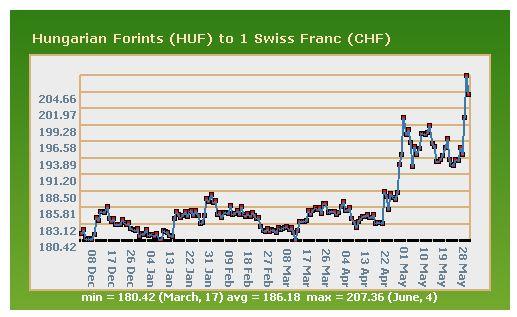

Apparently a significant number of Hungarians have historically taken out mortgages denominated in Swiss Francs. They liked the low interest rates those mortgages offered. Unfortunately over the last 6 months the Forint (Hungarian currency) has gone down against the Swiss Franc. See the 6 month chart below:

At the time of this writing, the Forint is trading at 204.33 Forints per Swiss Franc. It was higher on Friday. More importantly, it is approximately 10% lower against the Swiss Franc since March. This means that all of those with Swiss Franc denominated mortgages suddenly owe approximately 10% more. They suddenly have to make payments that are approximately 10% higher.

Hungary is worse off fiscally than the US. Can you imagine what it would do to the US real estate market if an appreciable number of home owners suddenly found that they owed 10% more than they had a couple of months ago? How would US citizens react if they had to make 10% higher payments in a high unemployment environment? Do you think Hungary’s real estate market may flounder? Do you think a good number of Hungarians are suddenly poorer? What do you think will happened as this gets worse?

The cumulative probability of default for Hungary is already 23.82%. The 5yr CDS spread is 400bps (up 91.5bps Friday alone). The current debt rating for Hungary is Baa1, but Moody's has a negative outlook on this. If previous market behavior is any indication, this is likely to worsen in the near future.

Do you think the extra Hungarian real estate problems due to the Swiss Franc mortgage problems will help Hungary’s credit ratings? Apparently the failure of a debt auction and a few negative comments by Hungarian officials started the recent credit slide. Can it cascade based on fundamentals such as increasingly troubled Swiss Franc denominated mortgages? A wild guess might be “yes”.

Before the IMF bailout in 2008, many mortgage were denominated in Swiss Francs. In 2006 and 2007 80% - 90% of new mortgages were denominated in Swiss Francs. After the bailout, banks virtually stopped making Hungarian mortgages denominated in Swiss Francs. A chart of the variety of interest rates is below:

If this wasn't bad enough, pre-recession the Hungarian real estate market was being pushed upward by foreign speculators. Many of these were Irish and Spanish. Need I say more?

Good luck trading.

May non farm payrolls +431k turned out to be lower than consensus and worse, most of the increase were made up from census job, rather than from private sector.

Euro fear is getting deeper. It's about Hungary. Euro tanked 1.6% during the session and moved below 1.2 for the 1st time since 2005.

Over the weekend, some positive progress on oil spill is reported BP. Its cap system was reported to be capturing 90% of the crude oil gushing from the crack at the sea bed. Should be a good sign on the speculative position on BP and Transocean. Will see on Monday.

Anyway, Hungary shouldn't be the last one in this European domino show which began being played out in March. I still remember vividly the troubles with Ukraine, Turkish banks in the mid of banking crisis in 2009... Hungary is weak, others may not be able to hang on for much longer either...

From Wiki:

Hungary:

- Capital: Budapest (beautiful place. one of the top 15 tourist destinations in the world)

- population: 10m

- GDP 2009: 130b

- joined EU in May 2004

- Privatization wave: The PM started the austerity program in 1995. The government privatization program ended on schedule in 1998: 80% of GDP is now produced by the private sector, and foreign owners control 70% of financial institutions, 66% of industry, 90% of telecommunications, and 50% of the trading sector (doesn't look really pretty to me)

- Real wage growth was negative from 2007. in the midst of 2008 banking crisis, the Hugarian National Bank raised interest to 11.5% and Hugarian Government took a 25.1b rescue package from IMF, EU and World Bank.

Seekingalpha/David White

Apparently a significant number of Hungarians have historically taken out mortgages denominated in Swiss Francs. They liked the low interest rates those mortgages offered. Unfortunately over the last 6 months the Forint (Hungarian currency) has gone down against the Swiss Franc. See the 6 month chart below:

At the time of this writing, the Forint is trading at 204.33 Forints per Swiss Franc. It was higher on Friday. More importantly, it is approximately 10% lower against the Swiss Franc since March. This means that all of those with Swiss Franc denominated mortgages suddenly owe approximately 10% more. They suddenly have to make payments that are approximately 10% higher.

Hungary is worse off fiscally than the US. Can you imagine what it would do to the US real estate market if an appreciable number of home owners suddenly found that they owed 10% more than they had a couple of months ago? How would US citizens react if they had to make 10% higher payments in a high unemployment environment? Do you think Hungary’s real estate market may flounder? Do you think a good number of Hungarians are suddenly poorer? What do you think will happened as this gets worse?

The cumulative probability of default for Hungary is already 23.82%. The 5yr CDS spread is 400bps (up 91.5bps Friday alone). The current debt rating for Hungary is Baa1, but Moody's has a negative outlook on this. If previous market behavior is any indication, this is likely to worsen in the near future.

Do you think the extra Hungarian real estate problems due to the Swiss Franc mortgage problems will help Hungary’s credit ratings? Apparently the failure of a debt auction and a few negative comments by Hungarian officials started the recent credit slide. Can it cascade based on fundamentals such as increasingly troubled Swiss Franc denominated mortgages? A wild guess might be “yes”.

Before the IMF bailout in 2008, many mortgage were denominated in Swiss Francs. In 2006 and 2007 80% - 90% of new mortgages were denominated in Swiss Francs. After the bailout, banks virtually stopped making Hungarian mortgages denominated in Swiss Francs. A chart of the variety of interest rates is below:

If this wasn't bad enough, pre-recession the Hungarian real estate market was being pushed upward by foreign speculators. Many of these were Irish and Spanish. Need I say more?

Good luck trading.

Monday, March 22, 2010

What makes it breaks it

Working on REIT again, I am having the opportunity to look at the failed models of General Growth (an internally managed Real Estate fund in US) and Centro (an Australian asset management company).

No doubt that these structures (including other property funds and trusts) all suffered from excessive leverage which ultimately pushed them either into bankruptcy or re-structuring when the property value falls, the process of levering up by these funds and the shocking cliff diving of their stock price performance in 2008 are quite intriguing.

I think the key reasons that pushed these vehicles over the cliff within such short period of time are primarily driven by the securitization model. The securitization model made these trusts and eventually broke their back.

General Growth represents a piece of the evolving CMBS market in US. Beginning in the 90s, upon taking over the failed balance sheet of banks suffered in the Savings and Loans crisis, the CMBS market quickly took steam. With a few billions in the beginning, it quickly evolved into a trillion dollar business by 2007. An active secondary market and strong liquidity for CMBS transfers into lower cost of capital for real estate borrowers. Coupled with rising valuation, the real estate investors took on the ride of no return...

Centro rode on a similar wave yet in a slightly different way... Centro started the fund management model as listed funds became popular in Australia. Through acquiring properties via private funds and selling funds public, Centro was able to arbitrage the dividend multiple and generate additional cash flow from acting as the asset managers for those funds... (look at today's Capitaland model)

As you see, the securitization model made the property market exciting, and lots of people rich during the process up until the credit crunch of 2008, when the market froze over. In a credit crunch, liquidation began with the more liquid assets such as the stock, bond, CMBS or anything that is traded. A fire-sale will send the CMBS price into a free fall which quickly eliminates much of the equity value within a very short period of time - this is what happened during the 2008. As CMBS prices drop to rock bottom, valuation of the property is "expected" to fall substantially and re-financing of the CMBS becomes near impossible because of the valuation gap, which pushes the property fund/trust into a liquidity crisis (admittedly for those over-leveraged like General Growth, investors quickly realized that a drop of 30% of the valuation already put the fund into insolvency), which in turn sends the equity to a point of no return. The case of MIREIT (Macarthurcook REIT in Singapore is an example which had $200mm of outstanding loan expiring in the mid of the credit crisis. The stock price dropped to basement level although its "theoretical" property valuation remained at $500mm).

Well, what makes it breaks it. Your strength is your weakness. well said. Lessons learnt: be cautious when others are greedy.

No doubt that these structures (including other property funds and trusts) all suffered from excessive leverage which ultimately pushed them either into bankruptcy or re-structuring when the property value falls, the process of levering up by these funds and the shocking cliff diving of their stock price performance in 2008 are quite intriguing.

I think the key reasons that pushed these vehicles over the cliff within such short period of time are primarily driven by the securitization model. The securitization model made these trusts and eventually broke their back.

General Growth represents a piece of the evolving CMBS market in US. Beginning in the 90s, upon taking over the failed balance sheet of banks suffered in the Savings and Loans crisis, the CMBS market quickly took steam. With a few billions in the beginning, it quickly evolved into a trillion dollar business by 2007. An active secondary market and strong liquidity for CMBS transfers into lower cost of capital for real estate borrowers. Coupled with rising valuation, the real estate investors took on the ride of no return...

Centro rode on a similar wave yet in a slightly different way... Centro started the fund management model as listed funds became popular in Australia. Through acquiring properties via private funds and selling funds public, Centro was able to arbitrage the dividend multiple and generate additional cash flow from acting as the asset managers for those funds... (look at today's Capitaland model)

As you see, the securitization model made the property market exciting, and lots of people rich during the process up until the credit crunch of 2008, when the market froze over. In a credit crunch, liquidation began with the more liquid assets such as the stock, bond, CMBS or anything that is traded. A fire-sale will send the CMBS price into a free fall which quickly eliminates much of the equity value within a very short period of time - this is what happened during the 2008. As CMBS prices drop to rock bottom, valuation of the property is "expected" to fall substantially and re-financing of the CMBS becomes near impossible because of the valuation gap, which pushes the property fund/trust into a liquidity crisis (admittedly for those over-leveraged like General Growth, investors quickly realized that a drop of 30% of the valuation already put the fund into insolvency), which in turn sends the equity to a point of no return. The case of MIREIT (Macarthurcook REIT in Singapore is an example which had $200mm of outstanding loan expiring in the mid of the credit crisis. The stock price dropped to basement level although its "theoretical" property valuation remained at $500mm).

Well, what makes it breaks it. Your strength is your weakness. well said. Lessons learnt: be cautious when others are greedy.

Sunday, March 21, 2010

Thank God I was born in 70s

For Saturday night entertainment, I watched Phoenix TV's 9pm live debate (hosted by 胡一虎). Again, it's about the property prices (According to Contrarians it should be indicator that price is about to fall - hope they are right). There were some insightful comments - there are certainly not short of insightful people not in control of power in China. Anyway, it was lively debate. It just got me into another point to be posted here.

I am not trying to be sarcastic by writing such a title. The reality is that those born in 80s, 90s, and maybe subsequent generations are, in general, less privileged than my generation (yes, 70s!). we had the chance of swimming naked in crystal water before growing up, being "the country's flowers" before going to college (if admitted), getting a job before leaving the school, paying affordable mortgages before getting married... Things just became dearer and dearer afterwards.

I have to pause and think how the next generation is going to prop up the social costs if there aren't significant structural changes made in the coming years. High property cost, as many blames, is driven by land cost and "excessive" local government spending. I don't know what's excessive or un-excessive, but clearly there is already stress in filling up the budget, at the time when the national GDP is still going strong at minimum 8%+.

How long this 8% can be here, when the rest of the world want to export as well? When US transformed itself into a consumer-driven economy, its GDP was growing at 3-4% when it was healthy. And it still ran on borrowing from the rest of the world.

Today's China is hard to sustain at 3-4%. Simple reasons i have include:

* there is a bigger government to sustain. Cost of sustaining the government should also include those "grey income" of the public servants as eventually productive labors have to bear it

* aging population and its healthcare costs

* less efficient use of resources as a result of wasteful state infrastructure investments in recent years and large sections of economy remained under state controlled enterprises

On the contrary, let's see what we have:

* less productive workers as a result of one child policy

* restrictive immigration policy, meaning less frequent exchange of capital and talents and potentially lower productivity

* other things - social inequality, lower education, etc...that points to a possibly lower productivity than today's US

Clearly GDP won't go on at 8%+ for ever. Is China sustainable when it's below 8%? what about 3-4%? To me those are structural issues that needs to be addressed. I have not found an answer so can only observe as it develops - that's what i can do as a "roadside economist" (watching events develop while standing on the road side).

I am not trying to be sarcastic by writing such a title. The reality is that those born in 80s, 90s, and maybe subsequent generations are, in general, less privileged than my generation (yes, 70s!). we had the chance of swimming naked in crystal water before growing up, being "the country's flowers" before going to college (if admitted), getting a job before leaving the school, paying affordable mortgages before getting married... Things just became dearer and dearer afterwards.

I have to pause and think how the next generation is going to prop up the social costs if there aren't significant structural changes made in the coming years. High property cost, as many blames, is driven by land cost and "excessive" local government spending. I don't know what's excessive or un-excessive, but clearly there is already stress in filling up the budget, at the time when the national GDP is still going strong at minimum 8%+.

How long this 8% can be here, when the rest of the world want to export as well? When US transformed itself into a consumer-driven economy, its GDP was growing at 3-4% when it was healthy. And it still ran on borrowing from the rest of the world.

Today's China is hard to sustain at 3-4%. Simple reasons i have include:

* there is a bigger government to sustain. Cost of sustaining the government should also include those "grey income" of the public servants as eventually productive labors have to bear it

* aging population and its healthcare costs

* less efficient use of resources as a result of wasteful state infrastructure investments in recent years and large sections of economy remained under state controlled enterprises

On the contrary, let's see what we have:

* less productive workers as a result of one child policy

* restrictive immigration policy, meaning less frequent exchange of capital and talents and potentially lower productivity

* other things - social inequality, lower education, etc...that points to a possibly lower productivity than today's US

Clearly GDP won't go on at 8%+ for ever. Is China sustainable when it's below 8%? what about 3-4%? To me those are structural issues that needs to be addressed. I have not found an answer so can only observe as it develops - that's what i can do as a "roadside economist" (watching events develop while standing on the road side).

Subscribe to:

Comments (Atom)